If you’ve ever opened your loan dashboard and immediately wanted to close the laptop, same. Student loans have this unique ability to turn even the most confident adult into someone who suddenly forgets how to do basic math. One minute you’re checking your balance, the next minute you’re Googling “Can I live on a boat?”...

Teacher TrainingThe Future of Student Loans: What Borrowers Should Know Going Into 2025

If you’ve ever opened your loan dashboard and immediately wanted to close the laptop, same. Student loans have this unique ability to turn even the most confident adult into someone who suddenly forgets how to do basic math. One minute you’re checking your balance, the next minute you’re Googling “Can I live on a boat?”

The truth is, student loans aren’t just a financial issue — they’re an emotional one. More than 43 million Americans hold federal student loan debt (Federal Student Aid, 2024). That’s not a niche problem. That’s a whole population trying to move forward while carrying something heavy on their backs.

And as we move into 2025, student loans are shifting. Policies are changing, repayment options are evolving, and borrowers need real information that isn’t confusing, sugarcoated, or written like an IRS document.

So let’s break it down in a way that feels human, clear, and actually helpful.

Why Does Student Debt Feel So Heavy? (It’s Not Just You)

If student loans feel stressful, it’s because… they are.

Unlike car loans or buying a couch you regretted from Wayfair, student loans affect every major life decision — when to move out, when to buy a home, whether to have kids, whether to change careers. According to a 2023 report from the Education Data Initiative, 60% of borrowers say loans delay major milestones, and nearly half say it affects their mental health.

And it makes sense:

You’re making payments on a degree you earned years ago, with interest that feels like it multiplies at night while you sleep. You’re paying for the “investment” in your future while trying to actually live in the present.

But here’s the important part — the landscape is shifting, and 2025 is shaping up to be a defining moment for borrowers.

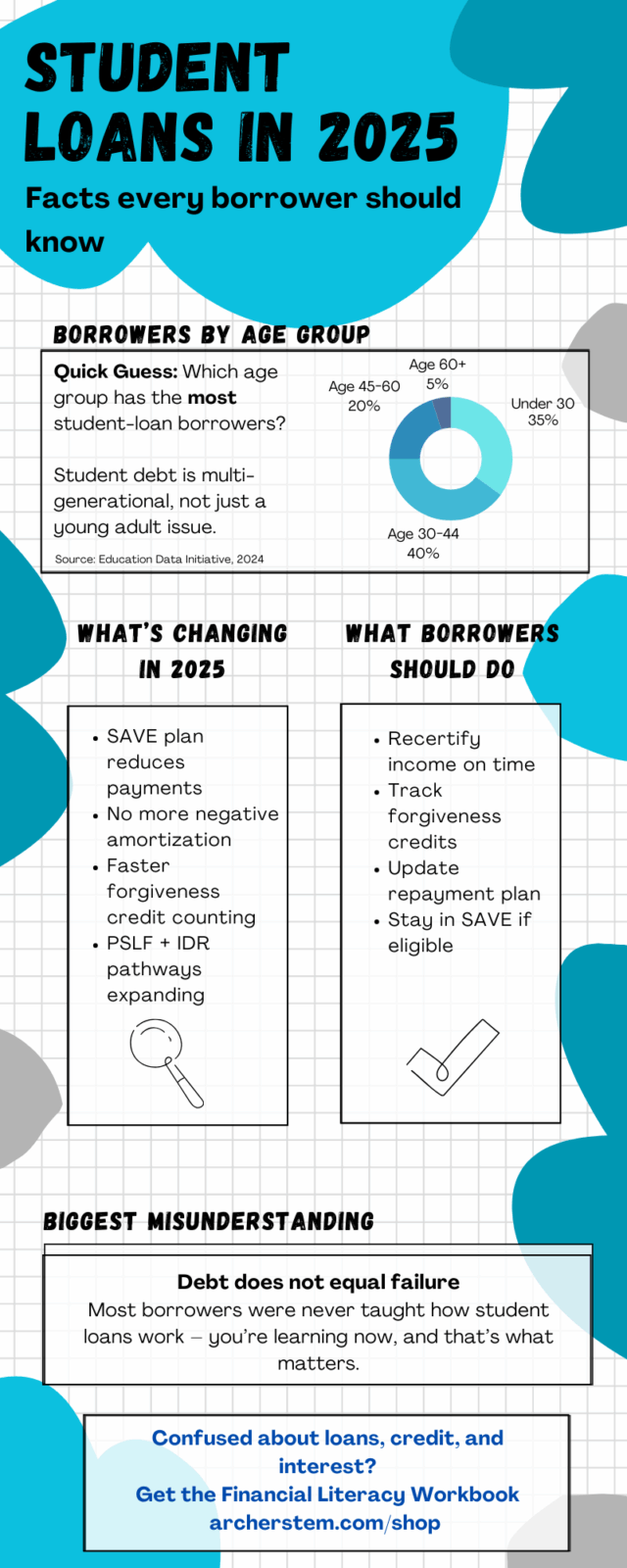

Repayment Is Changing: What Borrowers Should Understand Now

Here’s the biggest shift: student loans used to be basically one-size-fits-all. You paid what you owed, interest capitalized, and the process felt unforgiving.

Now we’re entering a new era — one with more flexible plans, more protection, and more opportunities to reduce what you owe.

The most impactful change is the rise of income-driven repayment (IDR) plans, especially the newer ones like:

-

SAVE Plan (Saving on a Valuable Education)

-

REPAYE adjustments

-

Income-driven recalculations

These plans cap your monthly payment based on your income, not your balance, which is huge. Under SAVE, some borrowers see payments drop to $0–$50 per month because discretionary income is calculated differently.

Not to mention, SAVE eliminates negative amortization — meaning your balance won’t balloon just because your payment doesn’t cover interest. (This is one of the biggest reforms in decades.)

According to Federal Student Aid, more than 7.5 million borrowers are now enrolled in SAVE, and the number is climbing every month.

The Biggest Question: Will Forgiveness Still Exist?

Short answer: yes, but differently.

The idea of blanket forgiveness caused a lot of political noise, but the reality is that targeted forgiveness is quietly expanding. And many borrowers don’t even realize they qualify.

Borrowers should continue to watch for:

-

Public Service Loan Forgiveness (PSLF)

-

Borrower Defense programs

-

Teacher Loan Forgiveness

-

IDR account adjustments

-

Closed school discharges

As of mid-2024, the Department of Education reports that over $160 billion has already been forgiven across these targeted programs — far more than most people realize.

Forgiveness isn’t gone. It’s just shifting into eligibility-based pathways instead of across-the-board cancellations.

What About Interest? The Part Nobody Likes to Talk About

Interest is the villain of the student loan story.

It’s the reason people feel like they’re paying but never progressing.

For context:

-

The average borrower has an interest rate between 4.99%–7.54% (CNBC, 2024).

-

Many borrowers end up paying 2–3x the original cost of their degree over time.

-

Over 17% are in default or delinquency (Education Data Initiative, 2024).

The good news: newer repayment programs are designed to protect borrowers from runaway interest, especially SAVE.

But the long-term solution is financial literacy — something most of us weren’t taught until adulthood (if ever). Understanding refinancing, consolidation, interest capitalization, and amortization should not require a PhD. Yet here we are.

So What Should Borrowers Do Going Into 2025?

Here’s the most realistic, beginner-friendly guidance:

1. Recalculate your income every year (on time).

This ensures you stay locked into the lowest possible IDR payment.

2. Don’t ignore your loan servicer’s messages.

They’re annoying, but they matter. Missing a form can cost forgiveness eligibility.

3. Check PSLF eligibility even if you think you don’t qualify.

Teachers, nonprofits, government workers — the PSLF program has forgiven over $60 billion since reforms in 2021.

4. If your interest is out of control, explore SAVE immediately.

It prevents negative amortization.

5. Track your forgiveness credits.

The IDR adjustment is giving borrowers retroactive credit, sometimes enough to erase loans entirely.

That’s it. Nothing overwhelming — just the basics that actually move the needle.

Let’s Talk About the Emotional Side (Because It Matters)

Millions of people carry student loans while juggling rent, groceries, careers, kids, and inflation. It’s not easy. And I think borrowers deserve more compassion than they get.

Some people carry shame about their debt. Some feel like they “should’ve known better.” Some feel hopeless, like their loans will exist forever.

But here’s the truth:

You didn’t fail. The system did.

And you’re not behind — you’re learning.

You’re figuring it out.

You’re educating yourself in a system that didn’t educate you on this part.

That is strength.

Why I Care About This — And Why It Connects to ArcherSTEM

Student debt is part of the reason I created ArcherSTEM’s workbook line. I met too many students — and adults — who were brilliant but financially lost because nobody ever taught them how money works.

Imagine how different things would be if schools taught:

-

interest

-

credit

-

debt

-

repayment options

-

investing basics

-

budgeting

-

taxes

We could prevent so much stress before it ever starts.

That’s why I believe financial literacy is a life skill, not an optional skill.

If you want practical, interactive, real-world activities to help teens and adults understand personal finance, credit, debt, taxes, and budgeting, I built a tool that makes it simple:

👉 Financial Literacy Activity Workbook

https://archerstem.com/product/financial-literacy-activity-workbook/

Or explore all ArcherSTEM resources:

https://archerstem.com/shop

Knowledge is financial power — and you deserve both.