Let’s be honest — most people don’t wake up one day saying, “Wow, I can’t wait to learn about index funds and tax-advantaged accounts. Pour that into my coffee.” No.Most of us just want less financial stress, more peace of mind, and a way to stop saying, “I really need to get my money together…”...

Teacher TrainingSmart Accounts, Bigger Savings: A Beginner’s Guide to Building Wealth

Let’s be honest — most people don’t wake up one day saying, “Wow, I can’t wait to learn about index funds and tax-advantaged accounts. Pour that into my coffee.”

No.

Most of us just want less financial stress, more peace of mind, and a way to stop saying, “I really need to get my money together…” every few months.

The truth is: wealth isn’t built by being perfect or by making six figures. Wealth is built by understanding a few basic tools that the average person was never taught in school. According to a 2023 FINRA study, only 34% of adults can answer basic financial literacy questions, and that number drops in younger generations.

But here’s the encouraging part — once you understand a handful of simple, beginner-friendly accounts, everything changes. Saving becomes easier. Emergencies feel less scary. Future goals (a home, college, retirement, or simply financial freedom) actually become possible.

Let’s break it all down in a way that feels human, normal, and doable — not like a finance lecture you didn’t sign up for.

Why Nobody Teaches This — and Why It Matters

You would think money management would be a part of the standard curriculum. Nope. Most adults learned about money from watching their parents struggle or Googling things at 2 a.m.

A Bankrate report found that 52% of Americans cannot cover a $1,000 emergency without borrowing. That’s not because people are irresponsible — it’s because they’ve never been given the tools.

That’s where modern savings and investment accounts come in. You don’t need to be rich to use them. You don’t need to be “good at math.” You just need to understand how they work and start small.

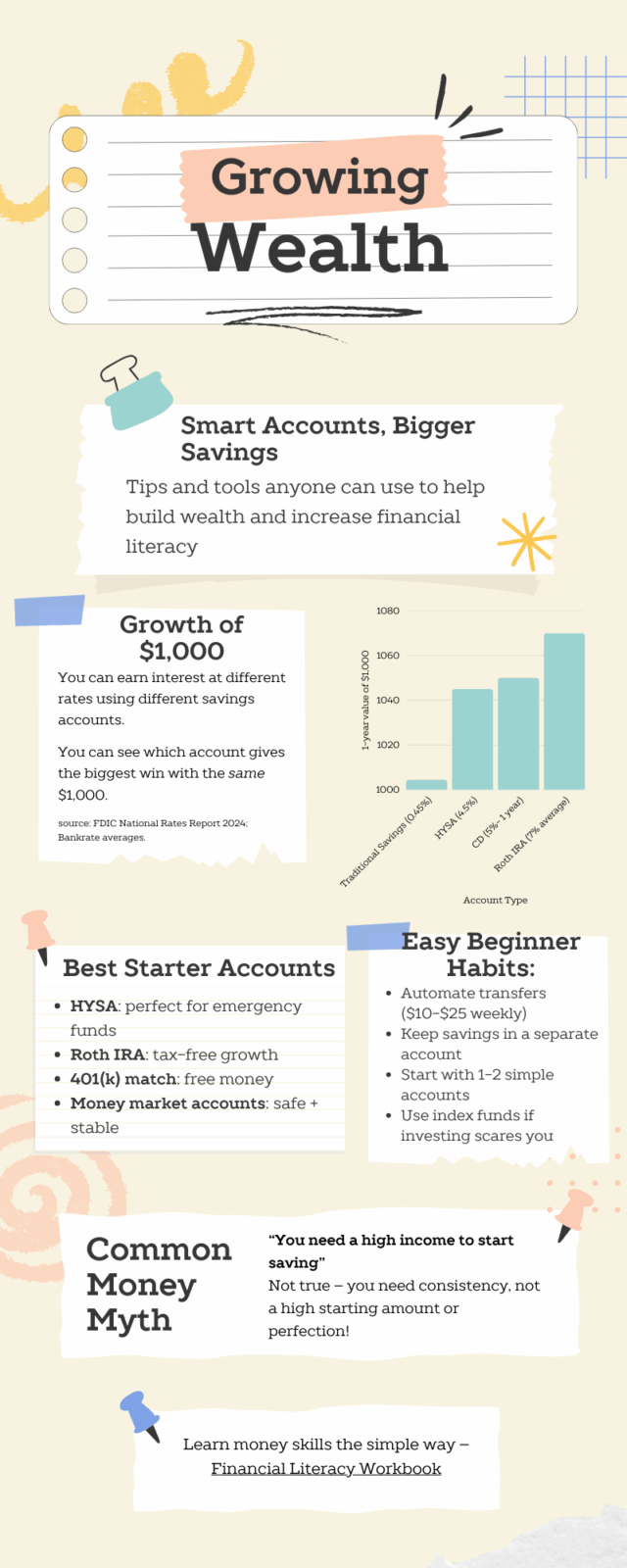

Let’s Start With the Easiest Win: High-Yield Savings Accounts (HYSA)

This is the simplest, most beginner-friendly place to start — and honestly, one of the best.

A high-yield savings account (HYSA) is basically a regular savings account…

except it actually pays you more than 10x the interest of a traditional bank, according to FDIC averages.

If you opened one in 2015, you probably didn’t get much.

If you open one now? You can get 4%–5% APY without doing anything fancy.

Why it matters:

-

Your emergency fund grows faster

-

Your money keeps up better with inflation

-

It requires zero investing knowledge

If you’re brand new to managing money, this is Step 1. No shame, no pressure — just saving smarter.

Roth IRAs: The One Account Everyone Wishes They Started Earlier

The Roth IRA is the Beyoncé of personal finance.

Quiet. Powerful. Respectfully above the rest.

A Roth IRA is a retirement/investing account where:

-

You invest money after taxes

-

Your money grows tax-free

-

You withdraw tax-free later in life

Translation: Uncle Sam does not touch your earnings. Not even a little bit.

For beginners, it’s perfect because:

-

You can contribute small amounts

-

You don’t need to understand stocks deeply

-

You can automate everything

-

You keep more of what your money earns

According to the IRS, the contribution limit for 2025 is $7,000 per year (higher if you’re over 50). But even if someone only puts $50–$100 a month, it compounds beautifully over time.

And here’s the best part — you don’t need to know what to invest in immediately. You can start with a target-date fund or a broad index fund (like an S&P 500 fund), which requires almost no effort.

Your 401(k): Not Just a “Work Thing” — It’s a Wealth Tool

Employers love to mention the 401(k) during onboarding when no one is mentally present. But this one is major.

If your employer offers a match, that is free money.

Like, literally free.

Example:

If they match 3%, and you earn $50,000, that’s $1,500 per year of free money — just for participating.

Even without a match, it’s still valuable because:

-

Contributions reduce your taxable income

-

It forces consistent investing

-

It grows automatically

The average person doesn’t realize that a 401(k) is often their largest wealth-building tool over a lifetime. Ignoring it means leaving tens of thousands on the table.

Okay, But I’m Not Trying to Be an Investor — What If I’m Just Trying to Survive?

Good question. And totally valid.

Not everyone is in a place where investing feels realistic. That’s where simple, low-risk accounts still play a huge role:

✔ Certificates of Deposit (CDs)

These lock your money in for a set period but offer high interest.

Bankrate reported that CD rates in 2024 were the highest in over a decade.

✔ Money Market Accounts

A middle ground between checking and savings — higher returns, but more access.

✔ Automatic Savings Apps

Even something like $10 a week builds momentum. Behavioral economists (Stanford, MIT) have found that small automated transfers drastically increase long-term savings.

These aren’t fancy, but they work — especially for people just starting out, rebuilding, or trying to stabilize their finances.

The Most Common Mistake People Make (And How to Avoid It)

The biggest mistake isn’t picking the wrong account.

It’s doing nothing.

Most people freeze because they think they need:

-

More income

-

More knowledge

-

More time

-

More confidence

-

Perfect budgeting skills

But research from the Consumer Financial Protection Bureau shows that small, consistent contributions beat large, inconsistent efforts — every time.

Wealth isn’t about timing. Wealth is about habits.

So instead of trying to overhaul your entire financial life in a weekend, start with these two steps:

-

Open a high-yield savings account.

-

Start automatic weekly or monthly transfers — even $20 counts.

That’s it. That one move changes everything in the long term.

What If You’re Starting Late? (Spoiler: You’re Not Too Late)

You wouldn’t believe how many people tell me they feel behind — parents, teachers, even college students who think they “should’ve started earlier.”

But money doesn’t have a deadline.

Whether someone starts at 17 or 57, the goal is the same: stability, peace, options.

Even starting small later in life makes a difference. A Vanguard study showed that investors who started at 40 but stayed consistent still built significant long-term balances.

The key isn’t age — it’s momentum.

I started ArcherSTEM because I kept meeting students and adults who felt embarrassed about money. They were smart, capable people who simply weren’t taught the basics. And honestly, it frustrated me. We shouldn’t need a finance degree just to understand credit scores, taxes, budgeting, savings, or debt.

So I created a workbook that makes all of this feel simple, visual, and interactive — not overwhelming.

If you want real-world, hands-on activities that help teens AND adults master these concepts…

👉 Check out the Financial Literacy Activity Workbook

https://archerstem.com/product/financial-literacy-activity-workbook/

Or browse all resources:

https://archerstem.com/shop

You deserve clarity. You deserve tools. You deserve financial confidence.