What Is Financial Literacy? Wealth Foundations, Career Economics & Practical Skills for 2025 Financial literacy is often described as “knowing how to manage money,” but that definition is far too shallow for the world we are entering in 2025. Financial literacy today is not just about budgeting or saving — it’s about understanding systems: how...

Teacher TrainingWhat Is Financial Literacy? Wealth Foundations, Career Economics & Practical Skills for 2025

What Is Financial Literacy? Wealth Foundations, Career Economics & Practical Skills for 2025

Financial literacy is often described as “knowing how to manage money,” but that definition is far too shallow for the world we are entering in 2025. Financial literacy today is not just about budgeting or saving — it’s about understanding systems: how income is created, how skills translate into money, how careers actually function, and how individuals can build stability in an unpredictable economy.

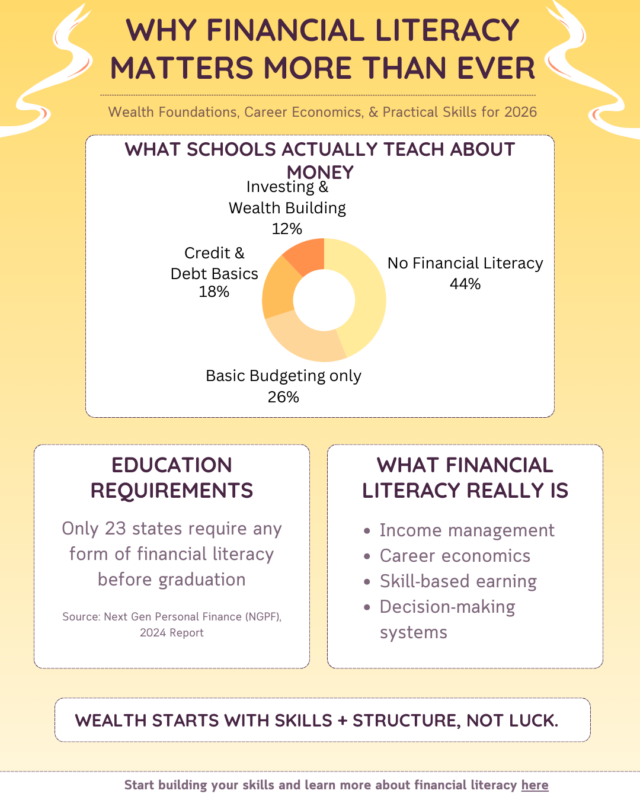

For decades, schools focused heavily on academic credentials while ignoring practical financial education. The result is a generation of students and adults who are intelligent, capable, and hardworking — yet financially insecure. Financial literacy fills this gap by teaching people how money, careers, and decision-making work in the real world.

According to the Federal Reserve, nearly 4 in 10 Americans cannot cover a $400 emergency expense without borrowing or selling something. This is not a motivation problem — it is an education problem.

What Financial Literacy Actually Means

Financial literacy is the ability to understand, manage, and apply money-related knowledge in everyday life. It goes far beyond knowing how to save or open a bank account.

True financial literacy includes:

-

Understanding how income is earned and scaled

-

Managing cash flow and expenses intentionally

-

Knowing how credit, debt, and interest work

-

Understanding taxes and deductions

-

Making informed decisions about careers, education, and investments

In practical terms, financial literacy allows someone to answer questions like:

-

How much do I really need to earn to live comfortably?

-

Which skills increase my income over time?

-

How do taxes affect my paycheck?

-

What is the tradeoff between college, certifications, or alternative paths?

-

How do I avoid financial traps that cost me years of progress?

Without these answers, people often make decisions blindly — choosing careers, loans, or lifestyles without understanding the long-term consequences.

Wealth Foundations: Income, Skills, and Systems

Wealth is often misunderstood as a number in a bank account. In reality, wealth is built on foundations, not luck or shortcuts. These foundations determine whether money grows, disappears, or never arrives in the first place.

Income

Income is the starting point of financial stability. However, not all income is equal. Hourly wages, salaried roles, commissions, freelance income, and business income behave very differently over time. Financial literacy teaches people how income works — not just how much they earn, but how predictable, scalable, and secure it is.

Skills

Skills are the engine behind income. In 2025, the most valuable skills are not always tied to traditional degrees. Skills in technology, finance, communication, data, operations, and problem-solving consistently outperform credentials alone.

Understanding which skills are in demand — and how to build them — is a core part of financial literacy.

Systems

Systems determine consistency. A person without systems relies on willpower; a person with systems builds momentum. Systems include budgeting routines, tracking tools, automation, savings plans, and decision frameworks.

People who understand systems are more resilient during economic downturns because they don’t rely on guesswork — they rely on structure.

Career Economics: Skills vs. Credentials

One of the most overlooked aspects of financial literacy is career economics — how careers actually produce income over time.

Schools often emphasize credentials (degrees, titles, GPA), but the job market rewards value creation. Financial literacy teaches individuals to analyze careers using economic logic:

-

What skills does this role require?

-

How rare or in-demand are those skills?

-

How does income grow with experience?

-

Can the skills transfer to other industries?

-

Is the income capped or scalable?

For example, two people may both earn $60,000, but one has skills that can scale to $120,000+ while the other is capped. Financial literacy helps people identify these differences early, before years are lost.

According to Georgetown University’s Center on Education and the Workforce, lifetime earnings vary dramatically by field, skill set, and career path — often more than by degree level alone.

Practical Skills Schools Don’t Teach

Most schools do an excellent job teaching theory. Where they fall short is practical application.

Commonly missing skills include:

-

Budgeting based on real-world expenses

-

Understanding paychecks, taxes, and deductions

-

Managing subscriptions and recurring costs

-

Comparing financial products (banks, credit cards, loans)

-

Evaluating job offers beyond salary

-

Planning for irregular income or side work

These are not advanced topics — they are everyday realities. Without them, students enter adulthood unprepared, relying on trial and error to learn lessons that could have been taught clearly and safely.

Why Activity-Based Learning Works Better

Financial literacy cannot be learned passively. Reading alone is not enough. Research consistently shows that hands-on, activity-based learning leads to stronger understanding and retention.

When learners:

-

Analyze real budgets

-

Compare financial scenarios

-

Track income and expenses

-

Evaluate career paths

-

Simulate decision-making

They develop confidence, not just knowledge.

This is why activity-based financial literacy workbooks and interactive exercises are so effective. They turn abstract concepts into real-life skills and allow learners to practice before real money is on the line.

According to the National Endowment for Financial Education, experiential learning significantly improves long-term financial behavior compared to lecture-based instruction alone.

Why Financial Literacy Is the Foundation of Self-Improvement

Financial literacy sits at the intersection of personal growth, career development, and mental well-being. When people understand money, they experience less anxiety, make clearer decisions, and gain more control over their future.

Self-improvement without financial literacy is incomplete. Motivation cannot replace systems, and ambition cannot replace education. Financial literacy provides the structure that allows other goals — education, entrepreneurship, family stability, and freedom — to become achievable.

The Bottom Line

Financial literacy is not about becoming wealthy overnight. It is about building clarity, stability, and long-term momentum.

In 2025, those who succeed will not necessarily be the most educated on paper — they will be the most financially literate in practice.

That is why financial literacy is no longer optional.

It is foundational.